There is a screen on your desk, or in your pocket, or open on your lap right now. Through it you can summon summaries, generate images, translate languages, write code, and conduct conversations with machines that respond with the fluency of a practiced essayist. The experience is frictionless and, in a very human way, magical. What it is not is free. Not in the financial sense, and emphatically not in the energetic one.

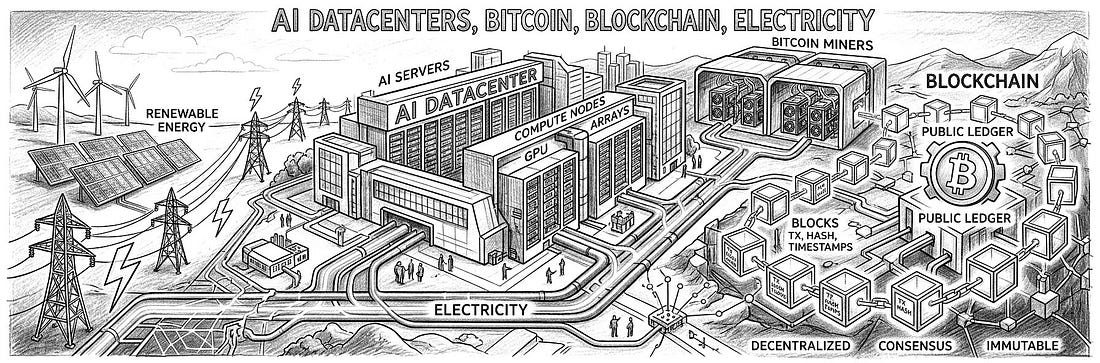

Every query you send to a large language model, every image rendered from a text prompt, every recommendation your streaming service generates, travels as a packet of electrons through copper and fiber to a building the size of a warehouse, where racks of graphics processing units run at temperatures that require industrial cooling systems to sustain. Those buildings drink electricity the way a steel mill does. And the electricity, despite what the press releases suggest, comes substantially from the same sources that have powered heavy industry for a hundred and fifty years.

The question is not whether artificial intelligence will transform civilization. It almost certainly will. The question is what we are burning to get there, whether we have been honest about the cost, and whether any of the alternatives we have are as ready as the people selling them claim.

The Scale of the Appetite Global data center electricity consumption reached approximately 415 terawatt-hours in 2024, roughly 1.5 percent of total global electricity use, according to the International Energy Agency.1 The IEA projects that consumption will roughly double by 2030, reaching around 945 terawatt-hours in its central scenario, a figure comparable to Japan’s entire annual electricity demand today. The agency acknowledges substantial uncertainty in this projection; the IEA’s four published scenarios cluster within roughly 100 terawatt-hours of that central figure, because much near-term data center supply is already committed through signed construction contracts.2 Data center electricity demand is growing at around 15 percent per year, more than four times the growth rate of all other sectors combined, a pace driven primarily by the rapid deployment of AI accelerator hardware.3 In the United States, the picture is sharper. American data centers consumed 183 terawatt-hours in 2024, representing more than four percent of total national electricity use.4 The IEA projects that by the end of the decade American data centers could consume more electricity than the country’s entire manufacturing sector, surpassing the combined load of aluminum smelters, steel mills, cement plants, and chemical facilities.5 A single large AI-focused facility already consumes as much electricity as a city of 100,000 households; the largest facilities under construction may require substantially more.6 Then there is cryptocurrency. Bitcoin mining consumed an estimated 138 terawatt-hours in 2024, comparable to the electricity use of Poland, approximately 0.5 percent of global consumption, according to the Cambridge Centre for Alternative Finance.7 The point is not a precise number. It is that proof-of-work mining, at any plausible figure in the range, represents a demand load comparable to a mid-sized industrialized nation, consuming power continuously and at scale, with no output other than cryptographic assurance.

The Energy Mix Is Not What the Logos Imply Every major technology company has a sustainability page. Most feature photographs of wind turbines and solar arrays, carbon neutrality pledges, and commitments to achieve net-zero by dates ranging from 2030 to 2040. The logos are green. The underlying energy mix is something else entirely.

In 2024, natural gas accounted for more than 40 percent of electricity powering American data centers, while coal supplied roughly 30 percent of the global data center mix, according to IEA estimates.8 Renewables provided approximately 27 percent of data center electricity worldwide. Nuclear contributed around 20 percent in the United States. The arithmetic is uncomfortable: more than half the electricity running the artificial intelligence revolution is generated by burning fossil fuels.

Nor is the trend moving cleanly in the right direction. The IEA projects that natural gas and coal together will meet over 40 percent of the additional electricity demand from data centers through 2030.9 Planned non-renewable capacity additions for data center power supply surged 71 percent between 2025 and 2026, while renewable additions grew only 2 percent in the same period.10 The structural reason is straightforward. Connecting a new power plant to the transmission grid requires paying network upgrade costs that vary enormously by fuel type. According to Lawrence Berkeley National Laboratory data covering the PJM region, natural gas grid-connection costs averaged $24 per kilowatt of installed capacity, against $253 per kilowatt for solar and $335 for offshore wind. Speed and economics favor fossil fuels. Ambition can be deferred; electricity demand cannot.

Google, which six years ago committed confidently to powering all operations from clean sources by 2030, now describes that goal as a “moonshot.” Microsoft calls its carbon-negative pledge “a marathon, not a sprint.” By Microsoft’s own accounting, its total greenhouse gas emissions for fiscal year 2023 were approximately 29 percent higher than its 2020 baseline, the year it announced its carbon-negative commitment, driven largely by data center expansion.11 Bitcoin’s energy profile is comparably difficult to characterize cleanly. A 2025 survey of mining operations found roughly 43 percent of the network running on renewables, 38 percent on natural gas, 10 percent on nuclear, and 9 percent on coal.12 The renewable figure is frequently cited by the industry as evidence of progress. What the industry prefers not to discuss is that Bitcoin miners require constant, baseload power. They do not operate only when renewables are generating surplus. When the wind does not blow and the sun does not shine, the miners run on whatever is available. The net effect on the grid is an increase in baseload demand, met, at the margin, by fossil generation.

What the Counterarguments Get Right (and Where They Fall Short) The technology industry is not without a defense, and parts of it are legitimate. AI model efficiency is improving rapidly. Energy required per AI inference task has been declining at a rate the IEA describes as unprecedented in energy history, and some researchers project that efficiency gains could partially offset the demand surge from expanded deployment.13 The most optimistic scenario in the IEA’s modeling shows demand growth significantly below the central case if efficiency improvements accelerate. That is a real possibility, not a dismissal.

The cost of solar power has also fallen to historic lows. Utility-scale solar in the best locations now prices at $0.012 to $0.019 per kilowatt- hour at auction, and the IEA projects renewables will meet nearly half of additional data center electricity demand between 2024 and 2030 as this buildout continues.14 Battery storage costs are falling along a similar trajectory. The renewables-are-too-slow argument that fossil- fuel advocates make is most accurate as a description of today’s grid; it becomes progressively less accurate as a description of the grid in 2030 or 2035.

The problem with leaning entirely on these counterarguments is timing. AI deployment is happening now, on today’s grid, at today’s capacity constraints. The efficiency gains and the storage buildout are projections. The new natural gas plants being approved today to power data centers will operate for 30 to 40 years. Infrastructure built for the 2020s problem will not disappear when the 2030s solutions arrive. Locking in fossil generation to bridge an efficiency gap that may close naturally is not a neutral interim measure. It is a commitment with a long tail.

The Shovels Sell for Billions The primary financial beneficiary of the AI energy surge is not the companies building applications or the enterprises deploying them. It is a single company that makes graphics processing units.

NVIDIA reported data center revenue of $30.8 billion in the third quarter of fiscal year 2025 (the quarter ending October 2024), up 112 percent from a year earlier. By fiscal year 2025, data center operations drove $115 billion of the company’s total revenue, against roughly $11 billion for its original gaming business, a near-complete inversion of its historical profile in under three years.15 NVIDIA’s share price rose more than 1,000 percent from January 2023 to mid-2025, briefly making it the most valuable company in the world. Its market share in AI accelerator chips reached approximately 86 percent by late 2025.16 During the California Gold Rush of 1849, the men who reliably made money were not the prospectors. They were the merchants selling picks, shovels, and denim. NVIDIA is selling the shovels for a rush that is consuming more electricity than most nations. The Gold Rush analogy eventually answers its own question: the landscape was transformed, and not always in ways the participants anticipated or desired.

Erin Brockovich and the Neighborhood Problem The energy abstractions become concrete when a data center arrives in your town. Nowhere is this better illustrated than in Loudoun County, Virginia, which hosts approximately 200 data centers and collected $875 million in tax revenue from them in 2024, $35 million more than its entire general operations budget.17 Loudoun is the success story the industry points to. What it does not represent is the median case.

In May 2026, environmental activist Erin Brockovich launched an interactive map inviting Americans to report concerns about AI data centers being built near their communities. Within a week, more than 1,800 reports had arrived from 47 states. Within a month, the number approached 4,000.18 A Gallup survey conducted around the same time found that 71 percent of Americans oppose AI data center construction in their local area, a disapproval rating exceeding that of nuclear power plants.19 Brockovich, who built her reputation holding Pacific Gas and Electric accountable for groundwater contamination in Hinkley, California, has been careful to note that she is not universally opposed to data centers. What she objects to is a recurring pattern of opacity. Projects move forward before nearby residents understand what is being built, what agreements have been reached with local utilities, or what the consequences will be for their electricity rates and water supply.

Consider the PJM electricity market, which stretches from Illinois to North Carolina and covers roughly 65 million customers. In the 2025-26 capacity market auction, PJM attributed approximately $9.3 billion in price increases partly to data center load growth. Average residential bills in western Maryland are expected to rise around $18 per month; in Ohio, around $16.20 Maryland utilities have not required data center developers to bear a proportionate share of the grid upgrade costs those facilities necessitate; the costs flow instead through standard rate cases to existing customers. This is not the outcome in every jurisdiction. Texas, for example, has experimented with large-load interconnection rules that assign more upgrade costs to the facilities requiring them. But Maryland’s experience is currently more common than Texas’s.

Water is a separate dimension of the same problem. Data centers require substantial quantities of water for cooling, though the precise volume varies significantly by cooling technology, local climate, and whether the facility uses wet cooling towers, closed-loop chillers, or direct-to-chip liquid systems. Training GPT-3 in Microsoft’s American data centers is estimated to have evaporated 700,000 liters of freshwater on-site, and more indirectly through power plant cooling.21 More than 160 new AI data centers have been built in the United States over the past three years in regions already classified as water- stressed. In Spain’s Aragon region, Amazon applied in late 2024 to increase its water consumption permit by 48 percent at three existing facilities. Aragon applied for European Union drought assistance in March 2025.22 In 2025, local opposition led to the delay or cancellation of projects totaling an estimated $156 billion in planned investment.23 That figure reflects not just community resistance but a governance gap: the permitting and siting frameworks that exist were designed for industrial facilities with well-understood footprints. A data center that draws as much power as a mid-sized city and evaporates water equivalent to a small river does not fit neatly into any existing regulatory category in most American states.

Bitcoin’s Fork in the Road Cryptocurrency is a separate but related problem, and it has a structural solution the industry has largely declined to apply to its most prominent product.

The energy cost of Bitcoin derives from its consensus mechanism: proof of work. To add a block to the blockchain, miners must perform enormous quantities of redundant calculation, each consuming electricity. The redundancy is intentional. It makes the chain expensive to attack, and Bitcoin’s advocates argue, with some rigor, that this computational cost is precisely what makes the currency’s immutability credible. The security model is not separable from the energy cost; they are the same thing.24 In 2022, Ethereum completed “the Merge,” switching from proof of work to proof of stake, in which validators are selected based on collateral held rather than computation performed. The network’s power consumption fell by more than 99.95 percent. The security model changed: Ethereum’s attack resistance now rests on economic deterrence rather than computational cost.25 Bitcoin advocates argue, not unreasonably, that this is a different and weaker security guarantee, and that Bitcoin’s energy expenditure is the price of the kind of finality that institutional finance requires. That is a coherent argument. It is not an argument that the tradeoff should be invisible or that the costs should fall on grid ratepayers rather than on network participants.

There are also efficiency improvements within the proof-of-work paradigm. Layer-2 networks built on top of Bitcoin process many transactions per unit of base-layer settlement, reducing the energy cost per economic unit of activity. Flared gas mining, in which miners convert methane that would otherwise be vented from oil wells to electricity, turns an emissions problem into a productive load. One estimate places the potential of this application at $16 billion annually in monetized gas.26 None of these improvements changes the fundamental arithmetic of the base protocol. They reduce the harm at the margin. The structural design decision remains.

The Grid That Parked Cars Could Power The preceding article in this series described a vision of autonomous pod networks running on sodium-ion batteries, drawing power from distributed solar and wind, and returning electricity to the grid when parked. The relevant passage for this discussion is the last part: the returning.

Vehicle-to-grid technology, in which parked electric vehicles discharge stored electricity back to the grid during periods of peak demand, is already in commercial deployment. Active pilots in California, Texas, and the United Kingdom now involve tens of thousands of enrolled vehicles. The value of such a distributed storage network scales with the number of vehicles. A fleet of millions of battery-equipped vehicles parked for 95 percent of their lives represents a storage buffer of extraordinary capacity, capable of absorbing surplus renewable generation and releasing it during peak demand.

This matters to the AI and cryptocurrency energy problem for a specific reason. The core argument for continued reliance on natural gas and coal to power data centers is that renewables are intermittent and that the grid requires dispatchable baseload power to maintain reliability. That argument is correct as a description of the current grid. It is not a description of what the grid must be. A grid backed by distributed storage, including vehicle batteries, changes the economics and the reliability calculus of renewable integration. The energy stored in a parked fleet of sodium-ion battery vehicles can, in principle, do for the evening peak what a gas peaker plant does now, without the emissions and without the fuel cost. And crucially: the infrastructure that makes this possible is the same infrastructure that decarbonizes transportation. The two transitions are not competing budget lines. They are the same investment.

What Governance Would Actually Look Like The technology industry’s energy problem is not primarily a technology problem. The technologies to address it, renewable generation, grid- scale storage, small modular reactors, and more efficient AI models, either exist or are in commercial development. The gap is in governance: the rules that determine how costs are assigned, how projects are approved, and how companies are held accountable to the commitments they have made.

Five specific interventions would close meaningful parts of that gap. First, large-load interconnection reform: require data center developers to bear grid upgrade costs proportionate to their demand, as Texas has experimented with, rather than socializing those costs across all ratepayers. Second, conditional permitting: tie data center construction approvals to verified clean power supply agreements that cover baseload hours, not just annual averages, removing the accounting fiction of renewable energy credits purchased in one market for facilities running on gas in another. Third, mandatory public disclosure of water consumption, emissions, and ratepayer impact assessments before permitting decisions are final, which is what Brockovich’s project is revealing the absence of. Fourth, accelerated SMR licensing: the NRC’s 18-month target for expedited small modular reactor approvals, signaled in 2025 executive orders, should be treated as a hard commitment rather than an aspiration, given that the first commercial units are needed before 2030. Fifth, a federal V2G interconnection standard: the vehicle-to-grid infrastructure described above requires interoperability rules that currently do not exist at national scale. Without them, the distributed storage potential of the EV fleet cannot be realized.

None of these is a prohibition. None requires choosing between artificial intelligence and the climate. They are the kind of coordinated industrial policy that the United States deploys when the political will exists. The political will is the variable that has not yet caught up with the problem.